Is Owning Both a Private Property and an HDB Possible?

Is owning both a private property and an HDB concurrently possible? Many would probably think that you can't or can't afford (which isn't technically wrong depending on the circumstances), but you can actually own both types of property concurrently.

But honestly, have you really thought about why someone would want to own two properties? Is it a high-flying ambition influenced by the wealthy and famous, or is it something that everyone should aim for at some stage in life, similar to how a parent plans for their children's future? It's crucial to understand this before making one of the biggest decisions of your life without due consideration.

Owning both an HDB flat and a private property in Singapore is an attractive prospect for many, but like any property purchase, it requires careful planning and strategic financial management. Let's delve deeper into the key strategies and considerations necessary for successfully achieving dual ownership.

My One & Only HDB

Owning both an HDB and a private property is a luxury and it definitely comes with some form of limitation. For starters, you are not allowed to own more than one HDB flat as opposed to private homes where you can own as many of them as long as you can afford the financial load.

Sequence Matters

The sequence in which you make your purchase matters, you can buy a private property after owning your HDB, but you cannot buy an HDB after owning a private property. If you own a private property and wish to buy an HDB, you would have to sell off your private property before acquiring the HDB. On top of that, in September 2022, the government introduced a new cooling measure that mandates a 15-month wait-out period for private property owners looking to right-size to an HDB flat.

Minimum Occupation Period (MOP)

The MOP is a critical factor in such a dual ownership model as you are prohibited from purchasing any private properties during this period.

As opposed to people who own two private properties which they can buy back to back, going the HDB then private property route means you have to wait at least five years before buying your private property. As you would see below later, more flats will actually be having a 10-year MOP, you should really consider this model with the missed opportunity cost of inaction during your MOP.

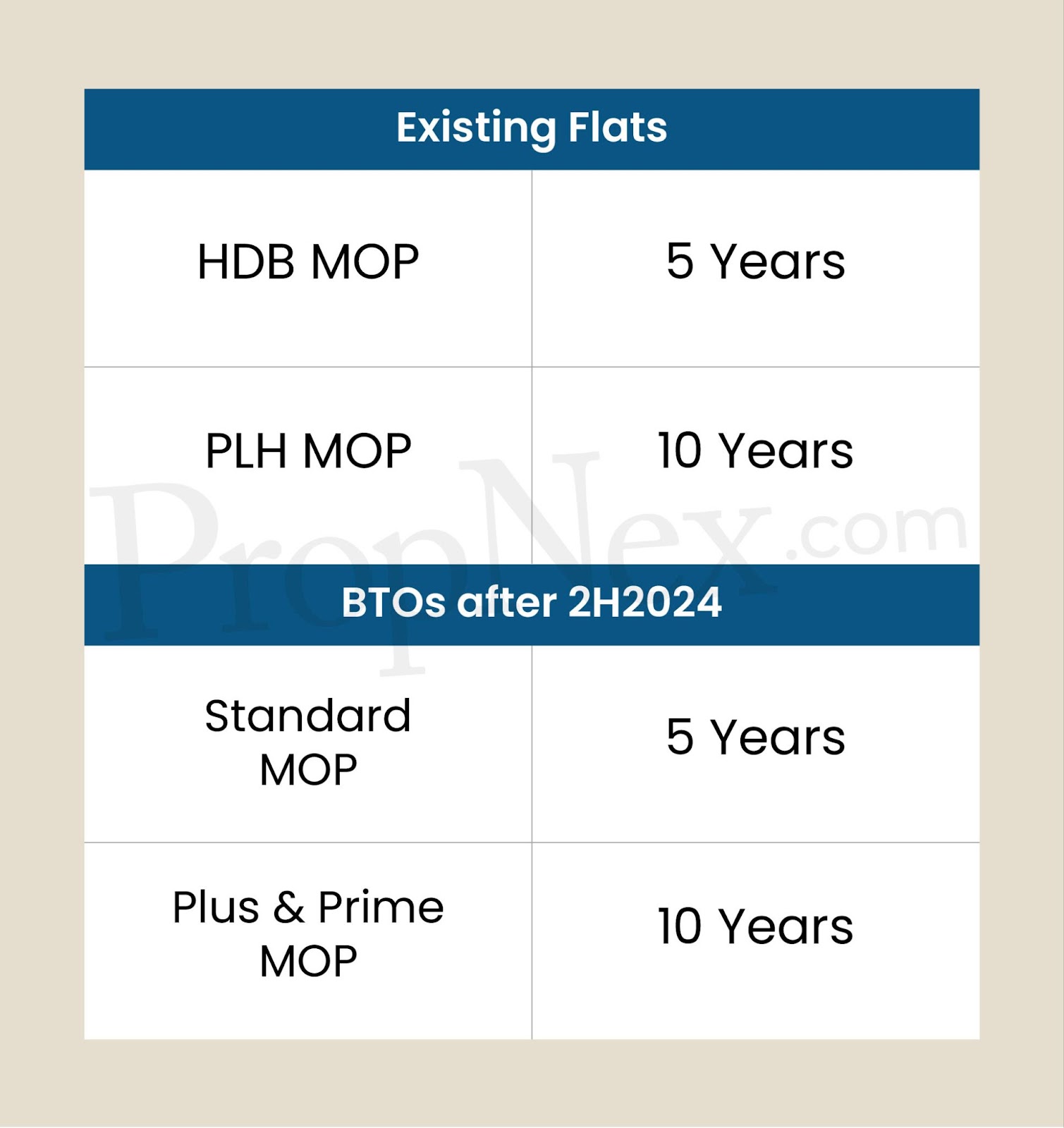

Generally, in today's market, most HDB's MOP is set at five years with the exception of prime location public housing (PLH) flats where the MOP is two times the duration at 10 years.

Announced during the National Day Rally 2023, BTOs built from the second half of 2024 onwards will be newly categorised to Standard, Plus & Prime classifications, replacing the current mature and non-mature estates. MOP for Standard housing will still be set at five years, whereas Plus & Prime houses will incur a 10-year MOP.

And for those who are thinking of getting a Plus or Prime home, you would actually have to wait for a good whole 10 years before you can actually purchase your second residential private property. Then again, homes classified as Plus or Prime would probably be the ones that would see more substantial gains. So it is important to plan for what you want to achieve out of this.

1. Paying ABSD

This method is the cleanest and most straightforward way of owning both types of properties, it is to pay for ABSD for the private property. The current rate for ABSD for a second property for Singaporeans is set at 20% of the purchase price. Look below to see the latest rates:

2. Break the couple up

Commonly known as decoupling, I'm sure more of you are more familiar with this term. It essentially entails having your spouse list themselves as an essential occupier as opposed to a co-owner, and it has to be done at the point of putting down your down payment for the BTO flat. This way, the essential occupier can purchase the private property without incurring ABSD. The downside of this method is that only the owner's salary will be taken into consideration for a loan and the monthly mortgage can only be deducted by their CPF account.

Once upon a time, you could simply transfer the share of one of the co-owners to the other but that option has been shut off by the government in 2016 - unless you have an extraordinary circumstance. So unless you did it from the start with your BTO, unfortunately, this method isn't viable for HDB homeowners.

3. Buying Under a Trust for Children

This method is definitely for those who are cash-rich as the property has to be purchased without the help of a mortgage loan or tapping on your CPF. To make things even more difficult, in April 2023, the government increased the ABSD from 35% to 65%. Remission of ABSD is possible if certain requirements are fulfilled. But it is still a hefty amount to fork out upfront to buy a private property using this method.

Another important thing to take note of is that the trustee (your child), has to be under the age of 21 years old.

This ultimately boils down to your end goals, on one hand the ability to own a property each in the public and private market diversifies your assets. We know from an exchange during a parliamentary session in 2022 that about 3% of HDB flat owners own at least one private residential property. Out of the bunch, about 45% of them do not reside in their HDB flat, and choose to rent the entire house out instead.

Even though there are several ways you can own an HDB flat and private property at the same time, you should also realise that it may result in differing outcomes. In terms of capital gains and the difficulty of achieving them, you should definitely speak to professionals who can further enhance your decision-making process, ensuring your property investments align with your long-term financial goals?. If you are interested in the intricacies of financing such an option, you should speak to a professional who can break down the figures for you based on your financial standings.

Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex.

For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Oh no!

Enjoy our Content?

If it is of any consolation, know that you are not alone in this real estate journey. Let us show you the way to make this journey an interesting and enjoyable one!

Suggested Reads

Upcoming Events

View more

You may like

Working Till 69 Won't Buy You A Longer Home Loan

July 21, 2026

Bank Of Mum & Dad 2: How To Help Your Child Buy A Home Without Risking Your Future

July 16, 2026

Resale Condo Market Watch in June 2026

July 15, 2026

When 8 Is Worth More Than 4: How Number Superstitions Shape Property Decisions

July 14, 2026

Cold Prospecting for Real Estate Agents: Making First Contact More Relevant

July 13, 2026