Manifesting Early Retirement

The idea of retiring early - spending your days chilling, pursuing hobbies or travelling - is very intriguing. But, achieving financial freedom in Singapore, a city known for its high cost of living, can seem like a distant dream. But what if I told you that you can retire early and not through some shady get-rich-quick scheme. The secret is...

Property!

Yup, you read that right. And I know what you're thinking, "I can't afford that, property is for the rich!". That, my friends, is nothing but a common misconception. In this article, we'll get into how property investment can be made safe and profitable. So, forget fancy investment ventures that keep you up at night, refreshing your phone just to see your crypto go bust. Property is a stable and secure way to build your wealth, and it will be the golden ticket to a comfortable retirement.

Before we get into the good stuff, I implore you to take the time to define what retirement means to you. How soon do you want to retire? The current official retirement age is 64. But perhaps you want to retire in your 50s, maybe even earlier. And what kind of lifestyle do you envision for yourself once you are retired? Are you going to travel the world? Pursue your hobbies? Spend time with loved ones? You need to determine these points so you can plan your retirement accordingly.

I hope you're not thinking that your CPF can give you your desired retirement lifestyle. If you are, let me explain why you shouldn't. Although CPF is an established retirement system, the reality is that CPF might not be (and probably isn't) enough.

In 2024, retired citizens can get a monthly payout of between $840 to $2,450 depending on how much they've saved in their CPF Retirement Account by age 55. This is classified into three levels of Retirement Sum (RS). Below is the breakdown.

| Level of Retirement Sum | Amount you've saved in your retirement account by age 55 | Estimated monthly payout (start receiving from age 65^) |

| Basic Retirement Sum (BRS) | $102,900 | $840 - $900 |

| Full Retirement Sum (FRS) | $205,800 | $1,560 - $1,670 |

| Enhanced Retirement Sum (ERS) | $308,700 | $2,280 - $2,450 |

Now, let's compare that to the cost of living in Singapore. Here is an estimate of a single person's monthly expenses:

- Food and groceries: $900

- Utilities: $130

- Public transport: $128

- Medical (provided one is healthy and not chronically ill): $50

- Shopping and recreational: $200

- Phone and internet plan: $60

In total, you're spending at least $1,468 each month for very basic needs. Mind you, even if you cut off shopping and recreation entirely, CPF's BRS tier still can't cover your monthly expenses. And this estimate was made under the assumption that you don't have to pay rent or mortgage, you don't have to support anyone else, you don't own a vehicle, and you live very moderately in general. Your expenses would look a lot different if you have children, or if you are taking care of an elderly parent, or if you want to go on vacation every now and then. Do you still think your CPF is enough to get by, let alone retire comfortably?

And remember, the monthly payout will only start once you reach 65 years old. That's totally fine if you're willing to wait. But if you're planning to retire early, you might want to keep reading.

Property is a tangible asset. Unlike cash and CPF, which lose purchasing power over time due to inflation, property values tend to rise with inflation. This means your investment keeps pace with the increasing cost of living.

Stocks, bonds, mutual funds and crypto aren't the best courses of action either. Though they offer high potential returns, they also come with a lot of risks, which can make it feel like a gamble. The market can be volatile, and external factors beyond your control can affect your investments. A bad quarter for a company you hold stock in or a global economic downturn can easily put you at a loss. Just look at FTX, a cryptocurrency company that went bankrupt not too long ago. Guess what happened to those who had FTX's crypto? Their accounts were frozen and they could not withdraw their assets. On the other hand, it's unheard of for property developments to be uncompleted in Singapore. So even if you're buying a Building Under Construction (BUC), your investment will still be safe. Ultimately, with property, you are in control of your investment. From choosing which units to buy and finding the right tenants to deciding when you want to sell, you are in charge.

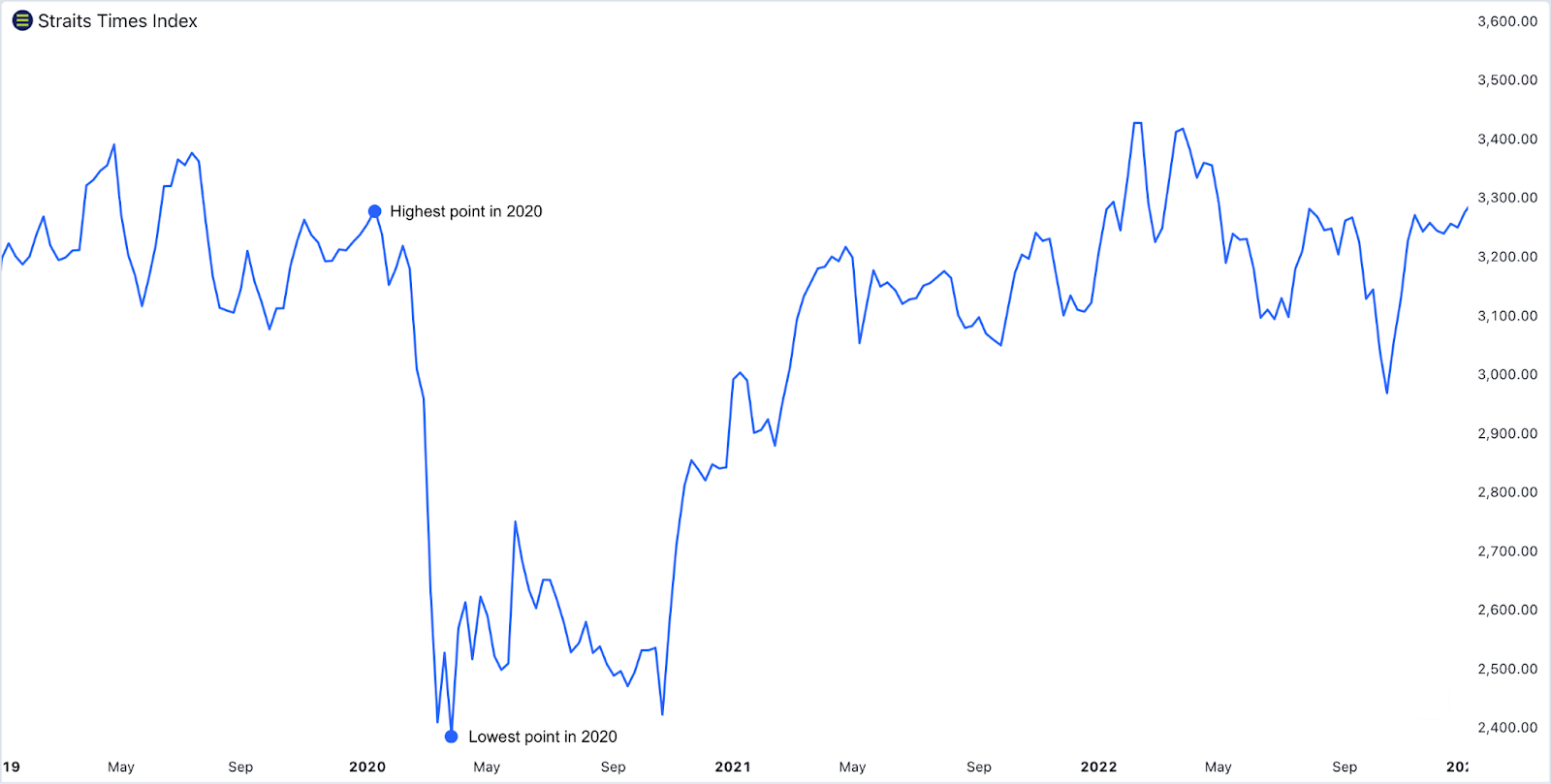

Still don't believe me? Let's take a look at the Straits Times Index (which tracks the 30 biggest companies on the Singapore Exchange) from 2019 to 2022. Overall, it's pretty clear just how much the stock market fluctuates. And when the world was hit by a global pandemic, the market crashed badly. The market kicked off 2020 at an average of S$3,238.38 and closed it at an average of S$2,852.71, meaning it experienced a downturn of nearly -12% throughout the year. What's even more concerning was the drop from its highest point, S$3,283.89, to its lowest point, S$2,208.42. That's a 32.75% decline in a mere few months!

And even though the market started picking up again towards the end of the year, it didn't quite reach the same level until the second quarter of 2021. If you're lucky, you can make a crumb of profit in the bullish points of 2022 (which can be tricky to predict due to drastic fluctuations). Moral of the story? The stock market is volatile and can change in an instant. Growth doesn't guarantee profit and if you're not out before the market dips, you'll probably face huge losses.

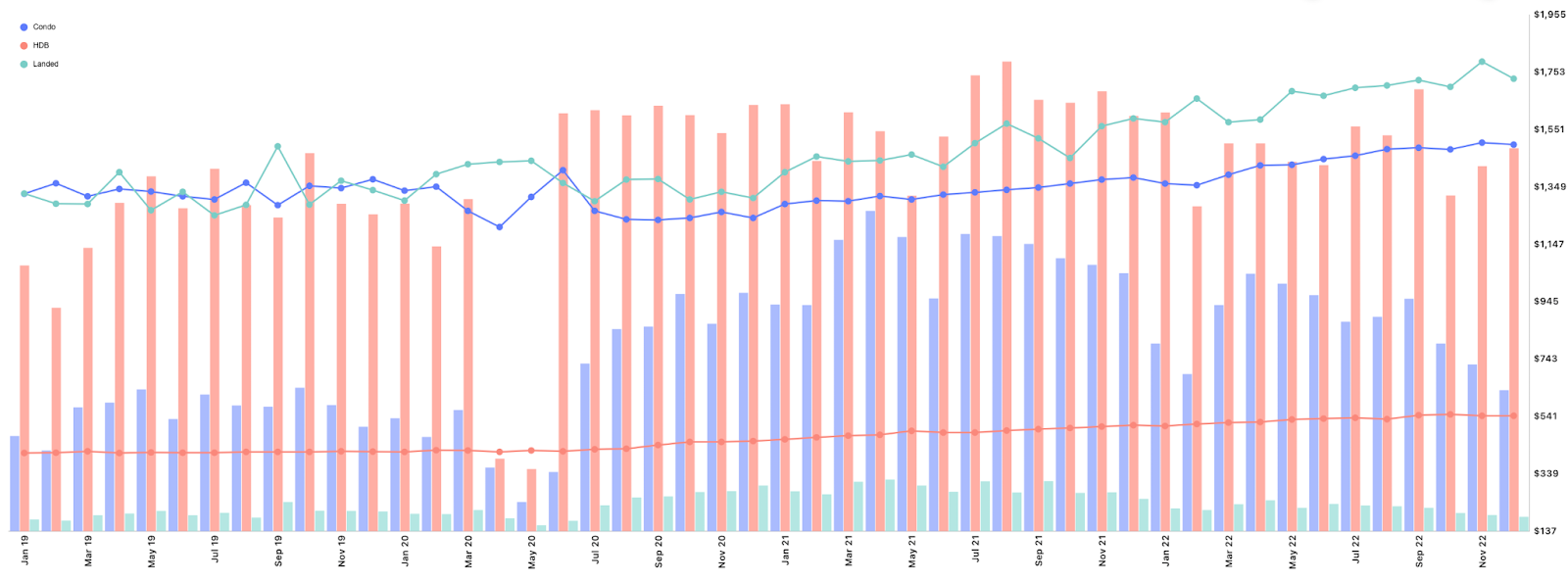

Meanwhile, Singapore's property market was relatively unaffected by the global pandemic. As you can see on the chart below, resale condos, HDB flats, and landed properties all remained stable with minimal fluctuations. They were even on upward trajectories! This just goes to show how stable Singapore's property market is compared to other investment schemes that fluctuate alongside unpredictable events.

To begin with, you'd have to buy a property. Of course, it is easier said than done right? However, with careful planning, it's definitely feasible. If you're worried about the capital, you can always look into smaller and more affordable properties to start with. Then, once the value has risen significantly since the purchase, you can sell it for a profit. This initial profit is the key to building your wealth and kickstarting your portfolio. The key is to keep increasing your net worth so that when you are retired, you have enough assets to support you for the rest of your days.

From here on, there are multiple paths you can take. Firstly, you can use the profit to upgrade your property. Perhaps you want to move to a larger home or a more desirable location. You can keep doing this as much as you'd like while you're still young and earning. Each time you upgrade to a more valuable property, you also accumulate wealth. Then, when you are ready to retire, you can sell your property and right-size it to a cheaper yet still comfortable home. You can then use the accumulated profits in your golden years.

And don't limit yourself to just one property. Having a diverse portfolio means you can have multiple exit strategies. You can choose to sell specific properties when the market is hot, maximising your return on investment. Or, you can opt for a more long-term approach by renting out your units. This generates a steady stream of passive income, which can pay for your living expenses and even fund your vacations during retirement years.

Do note that your age plays an important factor here because it will affect your mortgage tenure (longer tenures mean smaller monthly repayments) as well as your earning capacity. Not so simple is it? But don't worry because there is a proper framework that you can follow if you keep reading.

Once you've become a seasoned investor, you will be able to easily diversify your portfolio with various developments including commercial and industrial. However, a residential development is most ideal when you're just starting out.

Hearing that, you might feel inclined to get a Build-To-Order (BTO) flat. However, resale HDB flats and private properties actually make better investments. This is mainly due to the long BTO process: 4 years to build and 5 years of Minimum Occupancy Period (MOP). In total, you'd have to wait 9 long years. One of my colleagues actually regretted getting a BTO. You can read more about his experience here.

On the other hand, resale HDB flats and private properties offer immediate occupancy, allowing you to leverage your investment sooner rather than later. This will save you a lot of time, but as expected, the upfront cost will be higher. However, it's totally worth it! Starting strong with a resale flat or private property will pay off very quickly because they tend to have higher capital appreciation. So, if you can afford to get these more premium developments, go for it. Otherwise, you can always get a BTO flat, which is still a good stepping stone to the real estate market. You can also click here to learn more about BTO.

Ultimately, the sooner you start building your wealth, the sooner you can retire. And early retirement IS possible! You just have to take action now. Dive into property trends and explore options that resonate with you. And, if you still feel unsure, you can always sign up for our Property Wealth System Masterclass to receive insights straight from the pros (including our CEOs)! It's time to manifest your dream of early retirement into a reality.

Views expressed in this article belong to the writer(s) and do not reflect PropNex's position. No part of this content may be reproduced, distributed, transmitted, displayed, published, or broadcast in any form or by any means without the prior written consent of PropNex.

For permission to use, reproduce, or distribute any content, please contact the Corporate Communications department. PropNex reserves the right to modify or update this disclaimer at any time without prior notice.

Oh no!

Enjoy our Content?

If it is of any consolation, know that you are not alone in this real estate journey. Let us show you the way to make this journey an interesting and enjoyable one!

Suggested Reads

Upcoming Events

View more

You may like

Bayshore Drive: Idyllic Homes In A New Precinct

July 22, 2026

Working Till 69 Won't Buy You A Longer Home Loan

July 21, 2026

Bank Of Mum & Dad 2: How To Help Your Child Buy A Home Without Risking Your Future

July 16, 2026

Resale Condo Market Watch in June 2026

July 15, 2026

When 8 Is Worth More Than 4: How Number Superstitions Shape Property Decisions

July 14, 2026

Prospecting Discipline: Building Daily Habits That Create Future Appointments

July 13, 2026